How does the “Big Beautiful Bill” affect tax strategy and estate planning?

Congress recently passed the President’s “Big Beautiful Bill,” a comprehensive tax law that introduces significant changes for individuals, business owners, and investors. While many taxpayers will benefit from reduced taxes and new deductions, several provisions include income-based limits and marriage penalties that can reduce their effectiveness. Most of the changes are extensions of the bill President Trump enacted in his first term, which will keep the lower tax rates permanent. They were set to expire originally.

Below is a summary of the most relevant changes that may impact your financial planning:

Expanded SALT Deduction (State and Local Taxes)

- The deduction limit increases from $10,000 to $40,000 per return beginning in 2025, through 2029.

- It phases down for households with modified adjusted gross income (MAGI) over $500,000 and drops back to $10,000 by $600,000.

- A marriage penalty remains: two unmarried filers can claim $80,000 combined, while married joint filers are capped at $40,000.

New Senior Deduction

- Taxpayers aged 65 and older are eligible for a new $6,000 deduction per person ($12,000 if both spouses are over 65), effective 2025 through 2028.

- The deduction phases out starting at $75,000 (single) and $150,000 (joint) and is eliminated at $175,000 (single) or $250,000 (joint).

Qualified Business Income (QBI) Deduction

- The 20% deduction for pass-through business income is now permanent.

- Starting in 2026, phaseout thresholds increase to approximately $275,000 for single filers and $550,000 for joint filers.

New Deductions for Tips, Overtime, and Car Loans (Available 2025–2028)

- Tips Deduction: Up to $25,000 of tip income; phases out between $150,000–$400,000 (single) and $300,000–$550,000 (joint).

- Overtime Deduction: Applies to the “half-time” portion of overtime pay; limited to $12,500 (single) or $25,000 (joint). Similar phaseout ranges apply.

- Car Loan Interest: Deduct up to $10,000 of interest for U.S.-assembled new vehicles. Phases out between $100,000–$150,000 (single) and $200,000–$250,000 (joint).

Capital Gains Planning Opportunities

Opportunity Zones

- Investors can defer capital gains by rolling them into a qualified Opportunity Zone fund.

- A 10% tax reduction applies after 5 years, increased to 30% for rural investments under the new law.

- After 10 years, gains on the Opportunity Zone investment itself are entirely tax-free.

- These changes are projected to save taxpayers $41 billion through 2034.

Planning insight: This is particularly attractive for business owners planning a liquidity event or anyone with large gains from the sale of appreciated assets.

Qualified Small Business Stock (Section 1202)

- The capital gains exclusion cap increases to $15 million or 10x the original investment, whichever is greater.

- Investors may now qualify for a partial exclusion after just 3 years, down from 5.

- Slightly larger businesses now qualify under expanded eligibility rules.

- Projected tax savings: $17 billion.

Planning insight: A powerful tool for entrepreneurs, investors, and startup founders, especially in tech and venture-backed sectors.

Estate Tax and Step-Up in Basis Enhancements

- The estate tax exemption increases to $15 million per person, indexed for inflation, with no expiration date.

- More than 99.8% of estates will avoid estate tax under the new thresholds.

- The step-up in basis at death remains, meaning heirs do not pay capital gains tax on appreciated assets held until death.

Planning insight: Consider shifting appreciated assets into taxable accounts to benefit from the step-up in basis and revaluate trust structures for long-term tax efficiency.

Planning Considerations

| Tax Planning | Adjust income to manage SALT and deduction phaseouts. |

| Retirement Contributions | Maximize pre-tax 401(k), IRA, and HSA contributions to reduce MAGI. |

| Charitable Giving | Use Qualified Charitable Distributions to reduce taxable income. |

| Business Planning | Evaluate entity structure to optimize QBI and Section 1202 benefits. |

| Capital Gains Strategy | Consider Opportunity Zones and QSBS for deferral or elimination of gains. |

| Estate Planning | Reallocate appreciated assets for step-up at death and reassess trust use. |

If you have questions about how these changes affect your tax strategy, investment planning, or estate plan, please don’t hesitate to reach out. We’re happy to walk through personalized strategies that make sense for your situation.

Drivers of Equity Returns Likely to Shift Going Forward

Predicting stock market returns is famously difficult, with so many variables – many beyond anyone’s control – combining in unpredictable ways to humble even the most knowledgeable experts at times. Bonds, to those with even a passing knowledge of how their math works, seem easier to analyze with confidence given their more predictable cash flows and reactions to interest-rate changes. While bonds may seem more “mathematical” in how their returns are generated, stocks are nonetheless governed by three factors that in fact are also quite straightforward.

Equities derive their gains (or losses) from dividends, growth in earnings per share, and fluctuations in valuation. How these three interplay over time can be difficult to predict, but we can identify obvious headwinds and tailwinds for each that stem from the broader macroeconomic environment.

Unpredictable shocks like the pandemic or Russia’s invasion of Ukraine can throw wrenches into the engine of the global economy, but once those effects become clear we can factor them into the longer-term equity return assumptions that influence our portfolio asset-allocation decisions.

We’ll give a quick refresher on how each return driver works, and then look more closely at how the changes to the overall global economic environment influence our expectations going forward versus what they were in the prior period beginning after the 2008-09 financial crisis.

Dividends are the payments a public company distributes to its shareholders from the profits that it earns. Some (usually rapidly growing) companies opt not to pay much, if any, of their earnings in dividends based on management’s belief that reinvesting those cash flows into the business to drive further profit growth can generate higher long-term returns for shareholders.

Earnings growth and valuation changes are related. Valuation, measured as the price-to-earnings multiple (P/E) reflects how much investors are willing to pay for a share of a company’s stock per unit of earnings. If a company earns profits of $1 per share and the share price is $20, the P/E multiple is 20x. The idea of what investors are willing to pay for a dollar of earnings is a useful framework. If a company’s earnings grow from $1 to $1.50 per share, and the P/E multiple remains at 20x, a company’s stock price would increase from $20 per share to $30 per share. This is how earnings growth contributes to rising stock prices (and it works in reverse, of course).

When it comes to valuations, however, investors are typically willing to pay more for a dollar of current earnings if they expect future earnings to be higher. And if investors perceive a risk to future earnings – from business challenges like increased competition or a declining industry, for example – they may pay a lower P/E multiple for that company. An example of this would be a company that manages to increase current earnings from $1 to $1.50 despite a dim outlook for future growth, and as a result the share price remains at $20. In this case, the P/E multiple would contract from 20x to 13.3x. Investor expectations about future earnings are the reason why earnings growth and valuation changes can be highly interconnected.

Back to the drivers of return: if investors are willing to pay more for a dollar of earnings in the future than they are today (e.g. P/E multiples expand) then stock prices will increase even if earnings remain flat. Though in truth a likely driver of investors’ willingness to pay more is positive expectations about earnings, and so the two can reinforce one another.

That said, positive earnings expectations aren’t the only reason investors might pay more for a dollar of earnings. At the broader economic level, interest rates and risk perceptions are drivers as well. When rates are lower, stocks have less competition from generally safer investments like bonds, and investors are typically willing to pay more for a dollar of earnings from stocks. On the other hand, if investors become risk averse, as they were through the 2008-09 financial crisis or the onset of the pandemic, their fear in owning stocks is expressed in the form of lower valuations and P/E multiples contract.

If you think of a dollar of earnings as a product you buy, it makes clear the timeless investment adage (from Warren Buffett and others) that stocks are the rare product that people hate when they’re on sale and love when they’re most expensive.

The Interest-Rate Environment Has a Big Influence on Equity Returns

Looking backward, the biggest driver of equity returns during the ultra-low interest rate and inflation regime during the decade from the start of 2014 through the end of 2023 was earnings growth, which accounted for a little more than half of the S&P 500’s approximately 12% annualized gain during the decade. Earnings per share nearly doubled over that period, or just shy of 7% annualized.

Meanwhile 12-month trailing P/E multiple climbed from 18.5x to 26.8x during the same span (meaning investors went from paying $18.50 per share for each $1 of the index’s earnings to $26.80). This accounted for roughly a quarter of the S&P 500’s 10-year gain. Dividends contributed roughly 15% to returns (multiplication effects among the three make up the remainder). History shows, however, that valuation changes tend to have less impact over longer periods, suggesting this period may have been anomalous. The chart below shows the contribution of each return driver by decade going back to the 1930s. Dividends by definition are always a positive contributor but the magnitude has varied widely, and earnings growth has been positive every decade except the 1930s. Valuations, meanwhile, have both contributed and detracted meaningfully in past decades.

Looking again at the past decade, the historically ultra-low interest-rate environment not only decreased competition to equities from safer investments like bonds (which helps justify higher valuations) but it also contributed to profitability and earnings growth because access to cheap capital reduces companies’ borrowing costs and encourages growth-oriented capital expenditures.

Looking forward, the inverse to points we’ve made about interest rates become more important given that we are now in a meaningfully higher rate environment than most of the past decade. The headwind to valuations from higher interest rates comes in the form of increased competition from lower-risk fixed-income investments that now boast higher yields, and because a common methodology of analysts who determine what they’re willing to pay for a stock is based on the present value of future cash flows. A higher interest rate in that calculation results in a lower valuation for the same level of future earnings.

Looking ahead we don’t expect P/E multiples to contribute to returns as they have in the past year or in past decades. With P/E multiples nearing 25x, valuations are elevated relative to history, and if one assumes inflation of 3%, history suggests a P/E of around 17x is appropriate. Therefore, in our base case we expect a mild contraction of valuations creating a modest headwind to equity returns, and flat P/Es (meaning valuations don’t change) would be a positive outcome in our view.

That leaves us with two horses to pull the return cart down the track: earnings growth and dividends. Dividends are even lower now than just over a decade ago at the beginning of 2013. The S&P 500 currently has a dividend yield in the neighborhood of 1.4% versus close to 2% a decade earlier. And for dividend yields to contribute more to returns would require an offsetting decline in valuations (which pushes dividend yields higher) so all we in aren’t likely to see much contribution from dividends.

That all said, if most of your return is going to come from a single horse, earnings growth is the horse you want. Over the long term, earnings growth has been about 6% and has been the largest driver of equity returns. After a lull in 2022, earnings growth picked back up last year – as the most anticipated recession ever did not materialize – to reach all-time highs, as the chart below shows. The big question looking forward is whether earnings will continue to accelerate in the near term amidst a “goldilocks” economic scenario (not too strong or too weak) or if the economy slows. Over the longer-term, which is the basis for our investment decisions, we think earnings could grow in the mid-single-digit range, with overall equity returns in the same range given the contribution from dividends being offset by valuations pulling back a bit. A more optimistic scenario is also plausible with equity returns reaching high single- or low double-digit levels. In fact, this is in line with long-term historical averages.

The rest of the context for our analysis of the drivers of equity returns is what it means for portfolio allocations. With lower-risk fixed-income and alternative investments generating much higher yields and potential returns now in early 2024 than just a few years ago, their appeal is greater now compared to stocks than it has been in a long while. We have to take that into account as we make portfolio allocation decisions. Some final context to the analysis of equity return drivers and how they impact our portfolio decisions (or any research topic for that matter) is to remind everyone that the macroeconomic situation changes both gradually and at times suddenly, and requires a consistent analytical toolkit. We give more weight to factors that can be assessed with higher confidence and over longer time frames, and with a healthy appreciation for the unforeseeable. These are reasons we don’t typically make big tactical portfolio bets and why we believe diversification is critical to long-term success.

Week Summary 9/23/22 – All Eyes on Me… (Jerome Powell)

The Federal Reserve met yesterday and raised the overnight Fed Funds target rate by 75bps to 3.00% – 3.25%, matching the market consensus. That part was no surprise… but the forecast for future Fed Funds rates was more hawkish than market expectations, and that put pressure on both front-end Treasuries and equities. The long end of the curve did rally on the news, furthering the yield curve inversion (at 52bps it’s the largest inversion since 1981).

In other words, there was no Fed pivot that the markets had hoped for that aided the rally in the summer.

The updated projection by the Fed shows the median rate reaching 4.25% – 4.50% by year-end. While not consensus, six participants have the rate peaking at 4.75% – 5.00% in 2023 – these are substantially higher projections than were made a few months ago.

Rate cuts are now projected to start in 2024, but this date keeps moving further out as well. It appears the markets are starting to believe the Fed will keep rates higher for longer. Not long ago, rate cuts were projected to start early in 2023!

The Fed now sees inflation as more stubborn than previously thought. In June they had projected inflation would move quickly lower, but that is no longer the case. They now project Core PCE to be at 4.5% at the end of this year, down from the current levels of 4.8%. They are also projecting Core PCE to still be at 3.1% at the end of 2023 and 2.3% at the end of 2024.

The Fed has mostly dropped the “soft landing” talk, but still does not project the economy to go into recession (but do they ever?). While it does not expect unemployment to rise substantially, it is projecting the unemployment rate to hit 4.4% in 2024. That is 0.7% higher than the current rate. There has never been a situation where the unemployment rate rose more than about 0.5% without the economy entering a recession.

That being said, the S&P 500 (and other indices) are back to extreme oversold conditions (per Bespoke). A relief rally would not be surprising at all given the circumstances.

Source: Aptus Capital Advisors, Bespoke

This material is prepared by Optivise Advisory Services, LLC and/or its affiliates for informational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. This material may only be distributed in its original format and may not be altered or reproduced without the prior written consent of Optivise. The opinions expressed reflect the judgement of the author, are as of the date of its publication and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Optivise to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Optivise, its officers, employees, or agents.

This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. All investment strategies have the potential for profit or loss. All strategies have different degrees of risk. There is no guarantee that any specific investment or strategy will be suitable or profitable for a particular client. The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy

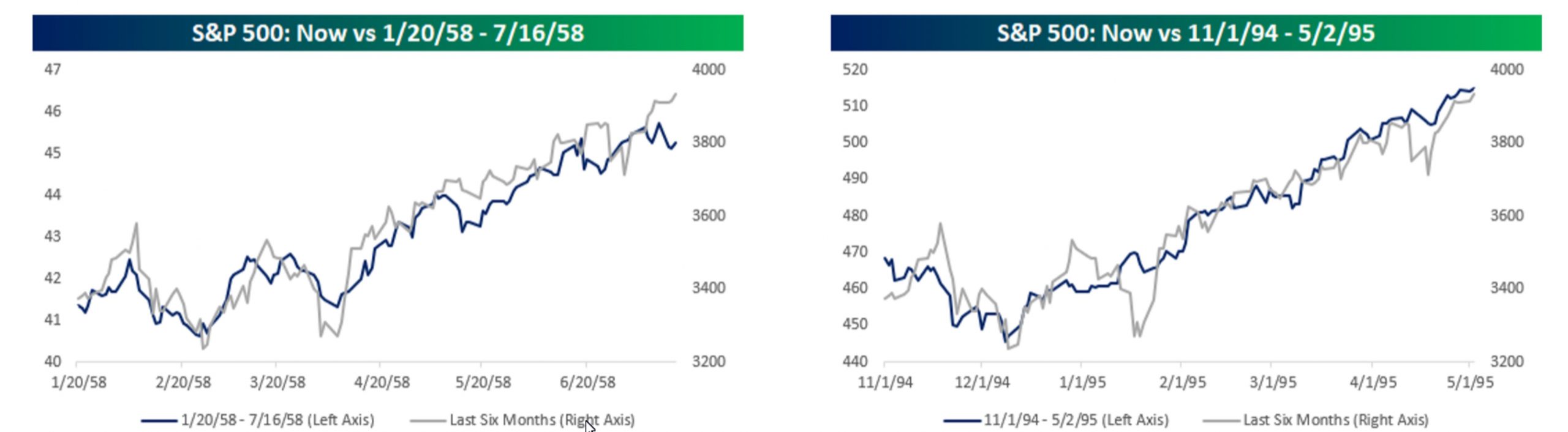

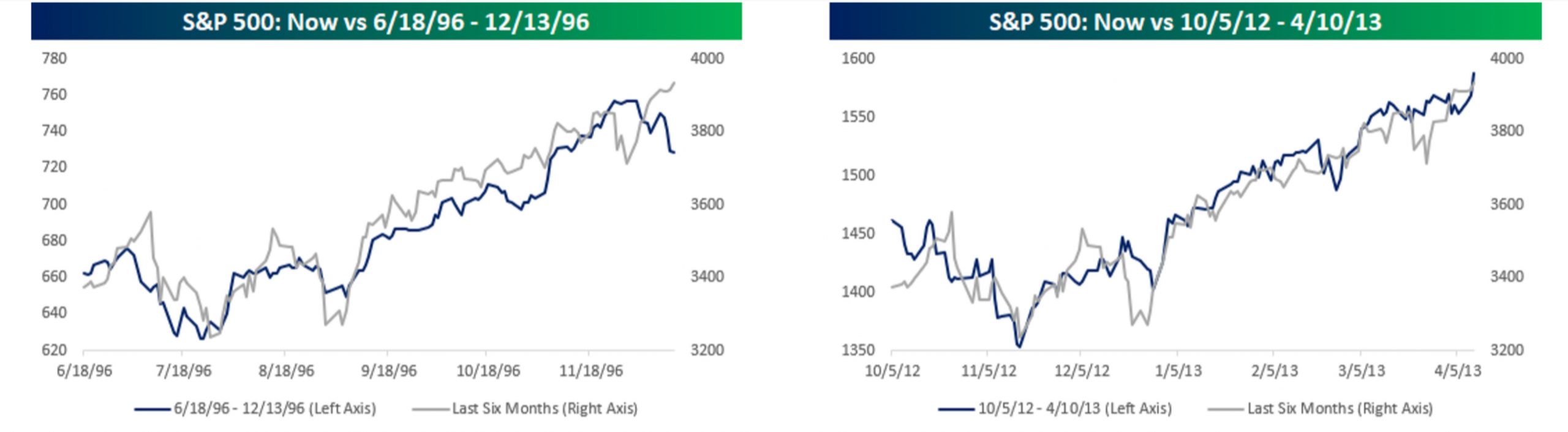

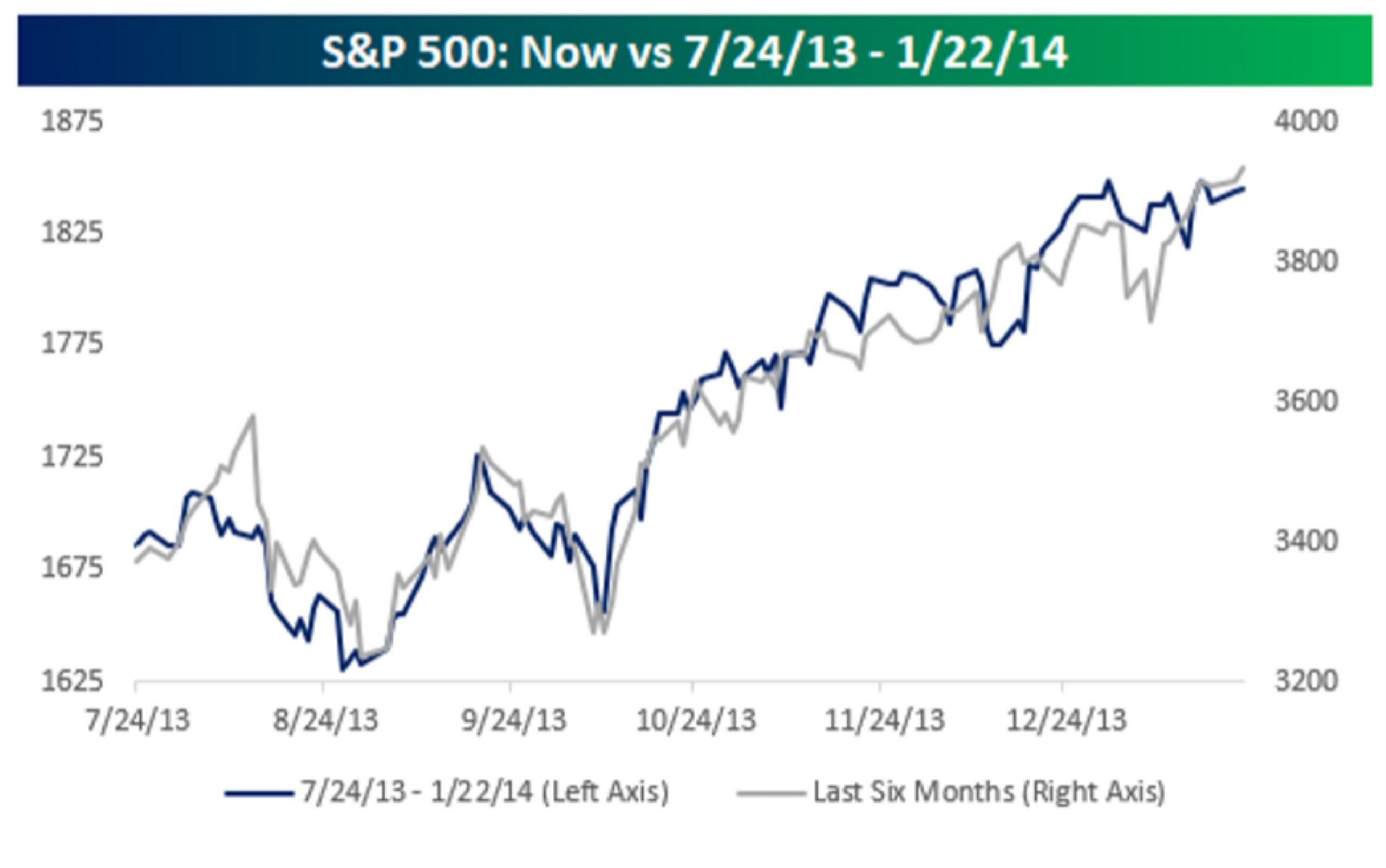

Starting to feel like DeJa Vu?

Quick warning – there are a lot of charts in this blog. I think they are well worth looking at though. I have seen a few articles comparing the rally since the March 2020 lows to the rally in 2009, and the two do look similar. Today, we are going to look at different time periods though. A recent piece from Bespoke compares the last 6-months to other 6-month rallies in the past. The results are pretty fascinating – take a look. Here are charts of 5 different periods since WWII with an overlay of the last 6-months in S&P 500 returns. The current rally is in gray and previous time periods in blue. Notice the similarities (they do not just look similar; they all have a correlation coefficient of 0.94 or higher)?

Before I state the next part, let me reiterate the typical investment disclosure: past performance isn’t indicative of future results. During the five previous rallies above, the average 1-year return was 22.9% with a median return of 25%. We can revisit a year from now to see how this one turns out.

Source: Bespoke

{kind=link}

Top Ten

Top Ten Things Everyone Should Plan On

Top Ten Things Everyone Should Plan On

The list I have prepared is based upon my life experience and not meant to be the “be all end all” of life’s decisions. It is meant to be a partial guideline that if one follows these basic principles, they will find that life’s other decisions come easier.

One – Center Your Life on Things Spiritual and be Charitable

This is not meant to be preachy because a relationship with the creator of the universe is and should be a very personal thing. If you choose to ignore things spiritual, then you are missing out on something very special. The creator of the physical wants to help you live a better life. Ignoring the advice of the one who made it all and understands it all seems silly and unwise. Listening for that guiding voice in every decision you make will help you make better decisions. When you listen to that voice you will hear the call to be charitable of your time and your blessings. You should have your Spiritual Luggage packed because you never know when you will be called to meet the Creator.

Two – Continually Educate Yourself and Keep Your Mind Active

As a child, we all hunger for knowledge. We explore, question, solve problems and approach every day with a certain awe and desire to learn something new. As we age, formal education becomes more of a burden than a desire for some. Some of us just want to get it over with and move on with our lives. The desire for independence is important for maturing, but we should never lose that desire to learn. Keeping the mind active with daily exercises. This can be done with brain teasers or memorization and recitation.

Three – Live Beneath Your Means

This one is probably the hardest for most of us. We all want to live comfortably and possess the same kinds of things that all our friends seem to have. Some people can find a way to do this to the extreme which I would have a hard time doing. One couple, both CPAs, chose to live in a tent and have a very minimal lifestyle while at the same time earning a good income. Another couple sold their home, purchased a semi-truck with a sleeper and lived on the road for many years while profiting from their modest lifestyle. We should all do everything we can to have a consistent portion of our income that is not needed for monthly expenses. Work out a budget that works and stick to it.

Four – Stay Healthy and Active

Diet and exercise, duh. When we are younger, we get used to not having to work too hard to stay healthy. As we age it seems that suddenly we find it harder and harder to be fit. A portion of every day should be devoted to physical activity. Find thirty minutes a day to do something that gets your heart rate up. Park in the spot farthest from the store. Take the stairs when you can. Find a way to eat only what you need to stay and maintain a healthy weight.

Five – Minimize Debt

If you could go through life never in debt, that would be very unusual in the USA. Remember the story of the CPAs that lived in a tent? They were never in debt, paid for the automobiles and other daily expenses without incurring debt. Once they had saved enough money to purchase a home, they did so. When they retired debt free, they lived comfortably off the interest from their savings. Most of us cannot imagine having to wait so long for things like homes and cars and choose to purchase them with credit. Then paying interest for the life of the loan, 5, 10, 15, 30+ years. You might be astonished to know how much interest charges we pay during our lifetime. The easiest way to get out of debt quickly is to focus on paying off the smallest outstanding debt first, then apply that monthly portion to the next largest debt. As you cancel out one debt and compound the payments with each eliminated account, soon all that will be left is the largest debt, and that one can be eliminated much sooner than the original payment contract. All it takes is making it a priority and sticking with the plan.

Six – Save For Unusual Expenses

Once you have your monthly budget in place, there will almost certainly be a time when unexpected expenses will occur. We should all have at least one month of normal family income in a liquid account like a checking or savings account. When you have one of these unusual expenses, pay for it out of this account and replenish the account as quickly as possible.

Seven – Save For Income Replacement

We never know if or when someone will lose their income. It can happen because of business reasons, health reasons, family needs, government interference, or something else. It is a good idea to have an account set aside that is reserved for this purpose. It should be a non-qualified investment account because it needs to be at least one year’s family income. Investment accounts can be liquidated quickly and can even be set up to allow them to be connected directly to a checking account. That can allow for direct transfers to and from the investment account. If you temporarily lose your income, you will draw from this account. Once you have reestablished your income, you would replenish this account.

Eight – Insure Wisely

There is an insurance policy for almost any kind of calamity you might face. Life, Auto, Health, Homeowner, Liability, Home Warranty, Accident, Cancer, Extended Warranty, Long-Term Care, Disability, Unemployment, just to name a few. Insurance needs change throughout your life. Don’t get over or under insured.

Nine – Share Your Wisdom

As you live these principles, you will start to notice how wise they are. You should not keep them to yourself but share your experience with others. Not in a braggadocio’s way, but in a helpful general informational way. Tell about your struggles and how you overcame them. Talk about how hard it was, not how easy it seemed afterwards. Encourage, don’t criticize. Love, don’t judge.

Ten – Save For Retirement Years

A portion of your income should always be saved for later. Someday you may want to be in a position that you no longer must work. It is a great position in which to be. Some people love what they do and will work for as long as they can physically and mentally do it. Other people want to retire and spend time in leisure activity enjoying travel or other things they could not do while employed. This should typically be the last stockpile you save into unless your employer has a match. In that case, save whatever amount will be matched by your employer until all the other stockpiles are fully-funded. Once your emergency and income replacement stockpiles are fully-funded, focus on this retirement stockpile and fund it to the limit.

{kind=link}

Holistic Approach Makes a Difference

In the tax preparation process, we will often find missed opportunities. Most people look to their investment adviser for returns on their money. This is an important quality, but sometimes tax avoidance can help one retain gains that they might have otherwise lost to taxes.

In the tax preparation process, we will often find missed opportunities. Most people look to their investment adviser for returns on their money. This is an important quality, but sometimes tax avoidance can help one retain gains that they might have otherwise lost to taxes.

Recently a couple took a large distribution from their IRAs and paid off their home and made some upgrades to their property. This distribution caused a $2,000 taxable event because their income was significant enough that their Social Security for that year was also taxable. Had they simply taken half of the distribution one year and the other half the following year, their taxable event would have dropped to $0. The amount of interest paid on the mortgage for those six months would have been approximately $200. Mathematically speaking, the client would have been ten times better off had they been able to follow our advice.

You cannot go back in time and change the past. In tax preparation, we must examine what our clients did, not what they should have or could have done. Tax Planning is the process of helping people make tax-efficient decisions every year. We strive to do this with our clients. Basically, there are three places that one’s savings will go:

-

– Client’s Estate

-

– Charity

-

– Taxes

Our default position is to help the client minimize taxes before, during, and after retirement.

Medicare and Health Savings Account

When do I have to register for Medicare?

When do I have to register for Medicare?

Something special happens as we approach the age of 65. We have a responsibility to register for Part A of Medicare when we become 65 years old. We have a 7-month window around our birth month in which to register. Three months before, our birth month, and the three months after.

What if I am still working when I turn 65?

A growing percentage of people are working well past age 65. This can make the decision a little more complicated when it comes to registering for Medicare. There are rules that differ based upon the size of company that you work for and what type of insurance coverage is in place.

Can I still contribute to my HSA after I am on Medicare?

You cannot contribute to a Health Savings Account and be on Medicare at the same time. If your employer has less than 20 employees, you must sign up for Medicare parts A, B, & D or Part C and you will no longer be on your employer’s plan. The only exception to this would be if your spouse is on your company plan and you want to keep her covered as a dependent. There may be some less expensive options depending on several factors.

Can I still contribute to my HSA after I turn 65?

This is one of those complicated situations. If your employer has less than 20 employees, then no. If your employer has more than 20 employees and it is allowed within the contracts of the health insurance, you may be able to contribute to an HSA. You would have to arrange to delay registration in Medicare and remain in your employer plan. It must be well documented so that when you retire or lose your employment you can register for Medicare and avoid the late registration penalties.

Are there any penalties for registering late in Medicare?

There is a 10% penalty applied to your Part B Premium for every year you do not register. If you are still employed and covered by your employer’s plan, this late penalty is waived. The penalty is simple, not compounded. If you delay by 3 years, then the penalty is 30% instead of a compounded 33.1%. This penalty usually is assessed for the rest of your life.

How Should One Approach The Medicare Dilemma?

Basic Process of Healthcare, Medicare and End of Life

Individual registers for Medicare at age 65

- Part A – Hospitalization (usually no cost)

- Part B – Doctor Visits and Specialists (Optional but if chosen the premium is deducted from Social Security)

- Part C – Medicare Advantage (This is a privatization of Part A & B and usually D. This can be chosen with several options and is either partially or fully covered by the standard Part B premium. Generally, Medicare Advantage Plans cover out-of-pocket expenses better than Standard Part A and Part B.)

- Part D – Prescription Drug Plans (These plans can be purchased individually or may be included in a comprehensive Part C Medicare Advantage Plan)

- Medicare Supplement Plans (These policies are designed to reduce or eliminate most out-of-pocket costs when used with Part A and B. There is an additional premium for these policies, and the premium is deducted from the Social Security payment)

Generally speaking, Medicare Options are best decided by a person’s financial situation.

- Part C should be chosen if you are a person of lower income, or for a person who prefers to cover out-of-pocket expenses and “self-ensure” for their expenses that are not covered by the insurance. Monthly premiums are usually lower.

- Parts A, B, and D with a Supplement Plan will be chosen by individuals who have plenty of retirement income or assets they don’t want at risk for health-related cost. There is little to no out-of-pocket expenses, but the monthly premium is significantly higher.

Scenario One – Low Income Person on Part C

- Admitted to Hospital because of serious illness

- Care is received

- After Hospital stay person leaves with a $4,000 bill

- Client pays hospital $20 a month

- Six months later, client passes

- Debt is most likely retired at death

Scenario Two – High Income Person on Parts A, B, D, with a comprehensive Supplement Plan

- Admitted to Hospital because of serious illness

- Care is received

- After Hospital stay person leaves most likely paid-in-full

- Six months later, client passes leaving assets to beneficiaries

Enrolling in Medicare is required when a person becomes 65 years old. A person has a 7-month window to enroll; three months before their birth month, their birth month, and up to three months after their birth month. In most cases, they must sign up for Parts A, B, and D or Part C with a drug plan included (or have other insurance in place). If a person does not sign up within that 7-month window, they will be assessed a monthly penalty for the rest of their lives once they do sign up. The longer the delay the higher the penalty.

Enrolling in Medicare is required when a person becomes 65 years old. A person has a 7-month window to enroll; three months before their birth month, their birth month, and up to three months after their birth month. In most cases, they must sign up for Parts A, B, and D or Part C with a drug plan included (or have other insurance in place). If a person does not sign up within that 7-month window, they will be assessed a monthly penalty for the rest of their lives once they do sign up. The longer the delay the higher the penalty.

Medicare does not cover costs associate with chronic illness (long-term care). Medicaid may cover costs of long-term-care if the person qualifies. Medicare covers most costs associated with Hospice Care.

Making Medicare choices should be thoughtfully made. There are a tremendous amount of options, lots of providers, lots of options within each provider, and rules about when you can make changes and when you cannot. Working with a Medicare Specialist that can guide you through the decision process is a wise choice. We will gladly help in anyway that we can.

Medicare decisions can feel like a maze of decisions. We will be glad to help navigate you to a well-informed decision.

What is up with that?

A lot of us look at the degradation of our society and wonder why. Why is the country headed away from God instead of towards him? Part of it is driven by the things we support, even if we do not know we are supporting them.

A lot of us look at the degradation of our society and wonder why. Why is the country headed away from God instead of towards him? Part of it is driven by the things we support, even if we do not know we are supporting them.

Did you know that companies sometimes use their profits to support things such as human trafficking, pornography, violent entertainment, gambling and such? Most businesses are not supporting anti-Godly activities because they believe in anti-Godly behaviors. Why then do they support such things? They support them because they believe it is in the best interest of company growth and profits. They are pushed into one direction or another based on how best to increase stock prices and stock ownership.

It is likely, in my opinion, that if we invest in companies that are supporting Godly things and there is enough of us, we can have an impact on the moral compass direction of Wall Street. Even if they don’t care one way or the other about morality, they will conform themselves in the best way possible to promote stock ownership. If Godly believers join together, the impact will be huge. There are a lot more of us and if money dries up for ungodly behavior and wells up for Godly behavior, businesses will clamor for Godliness even if it is only for profit.

If we invest our dollars in these companies, are we not also supporting the things they support? Even though we might have our money in mutual funds or a 403(b)/401(k), those monies are invested in companies. Isaiah 5:20 says, “Woe to those who call evil good and good evil…” I believe that we shouldn’t invest in evil and call it good or claim that it is good when it’s really not. Do you agree? Do you know what your investments support? If there was a way to find out if your investments are “clean”, would you want to know? Even some mutual fund companies that claim to have a high moral and ethical posture, may not actually be “clean.”

There is a web-based service that can impartially show what an investment supports either directly, or indirectly. We want to help you have a “clean” investment option. I believe that we can show Wall Street that biblical values are important if we start putting our money into the hands of companies that support biblical principles. Wouldn’t the country be a better place if corporate America started supporting biblical principles? If you agree, let me know. I will do what I can to help you communicate your biblical principles with the dollars you invest.

What do you profit from with your investments?

Did you know that some companies have some of their profits enhanced from things that are against scripture, such as pornography, violent entertainment, gambling and such? If we invest our dollars in these companies, are we not also profiting from those things? Even though we might have our money in mutual funds or a 403(b)/401(k), those monies are invested in companies. Isaiah 5:20 says, “Woe to those who call evil good and good evil…” I believe that we can’t invest in evil and call it good or claim that it is good when it’s really not. Do you agree? Do you know what your investments support? If there was a way to find out if your investments are “clean”, would you want to know? Even some mutual fund companies that claim to have a high moral and ethical posture, may not actually be “clean.”

Did you know that some companies have some of their profits enhanced from things that are against scripture, such as pornography, violent entertainment, gambling and such? If we invest our dollars in these companies, are we not also profiting from those things? Even though we might have our money in mutual funds or a 403(b)/401(k), those monies are invested in companies. Isaiah 5:20 says, “Woe to those who call evil good and good evil…” I believe that we can’t invest in evil and call it good or claim that it is good when it’s really not. Do you agree? Do you know what your investments support? If there was a way to find out if your investments are “clean”, would you want to know? Even some mutual fund companies that claim to have a high moral and ethical posture, may not actually be “clean.”

We have a web-based service that can impartially show what an investment supports either directly, or indirectly. We want to help you have a “clean” investment option. I believe that we can show Wall Street that biblical values are important if we start putting our money into the hands of companies that support biblical principles. Wouldn’t the country be a better place if corporate America started supporting biblical principles? If you agree, let me know. I will do what I can to help you communicate your biblical principles with the dollars you invest.